Where are Interest rates headed?

Thursday Nov 09th, 2023

Compliments of the BDC, Nov 2023 Economic letter

Where are interest rates headed?

In its last two rate announcements, the Bank of Canada opted to maintain the status quo, keeping its key rate at 5.0% since July 12. Now that the U.S. Federal Reserve has also hit pause on its rate hikes, many are wondering if we could actually be done with tightening for this cycle. Could we even expect the Canadian central bank to lower rates soon?

Is the Bank of Canada done with rate hikes?

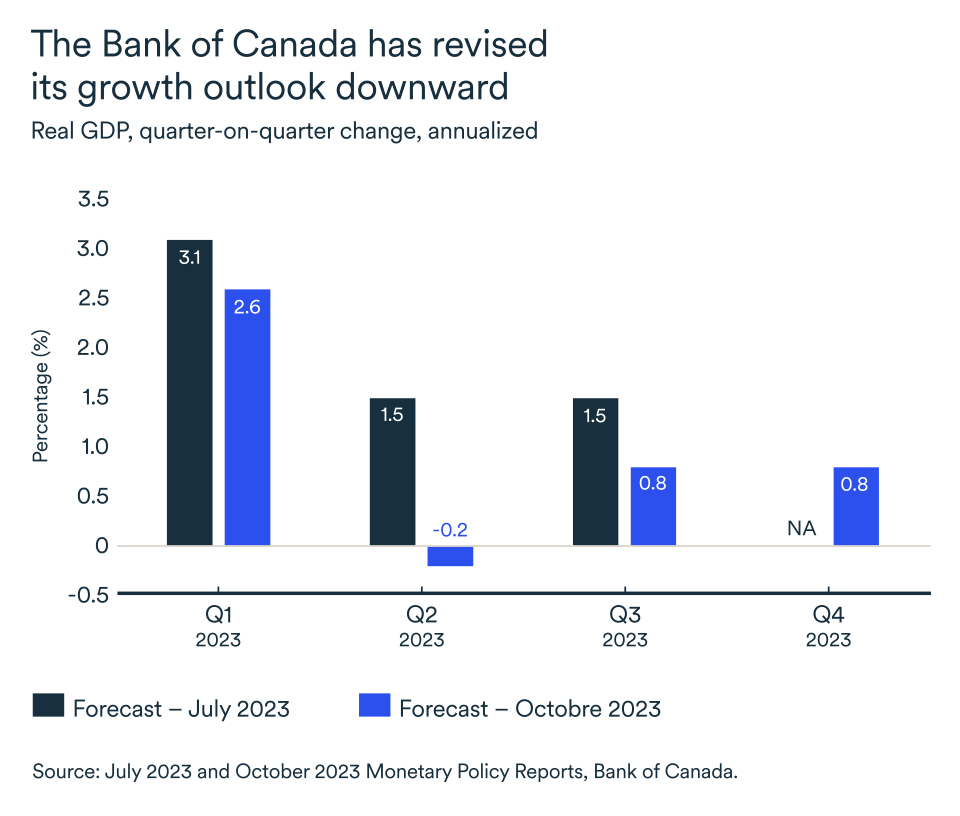

According to the Bank of Canada, the economy is set to slow much more than it had anticipated just three months ago. In July, the central bank was forecasting economic growth of 1.8% in 2023 and 1.2% in 2024. By October, the bank’s outlook had been updated to 1.2% and 0.9%.

Despite the downward growth revisions, Governor Tiff Macklem reiterates at every rate announcement that the bank is ready to proceed with further hikes if necessary. The Bank of Canada's mandate is price stability, not economic growth, and it remains focused on seeing inflation come down to its 2% target.

Enlarge the table

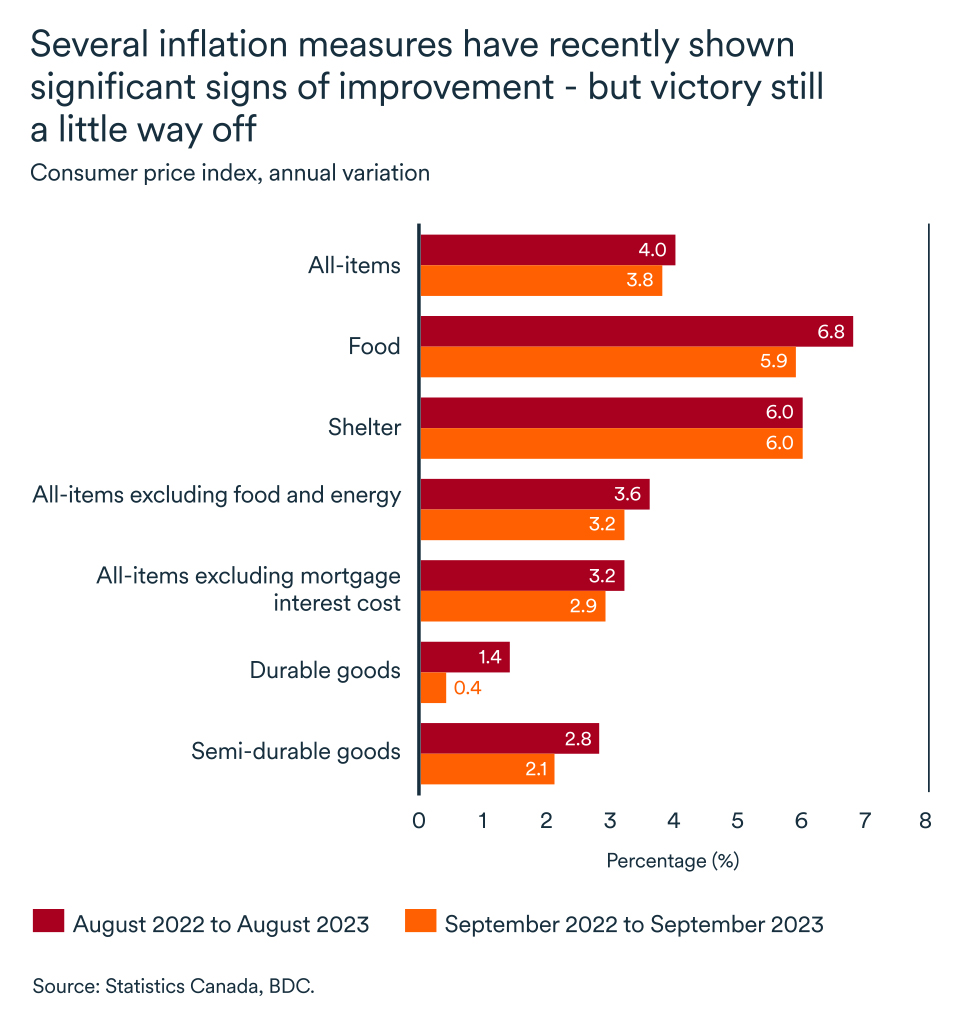

Enlarge the tableAlthough risks remain, inflationary pressures appear to be easing

While economy was slow to react in the early stages of the tightening cycle, the inflation picture turned more positive in September.

The consumer price index edged down to 3.8% in September from 4% in August. While this was still above the Bank of Canada’s target range of 1-3%, monetary policy seemed to be working. Price increases for interest-rate sensitive items, such as debt-financed and discretionary goods, had returned to the target range.

While growth remains solid in the U.S., it’s stagnating in Canada. The differential between U.S. and Canadian rates could widen further if the Federal Reserve decides to hike again. Another increase could have a negative impact on Canada's fight against inflation because the Canadian dollar would be further devalued against the U.S. greenback, making Canadian imports more expensive.

Enlarge the table

Enlarge the tableHigh inflation and high interest rates, the two go hand in hand

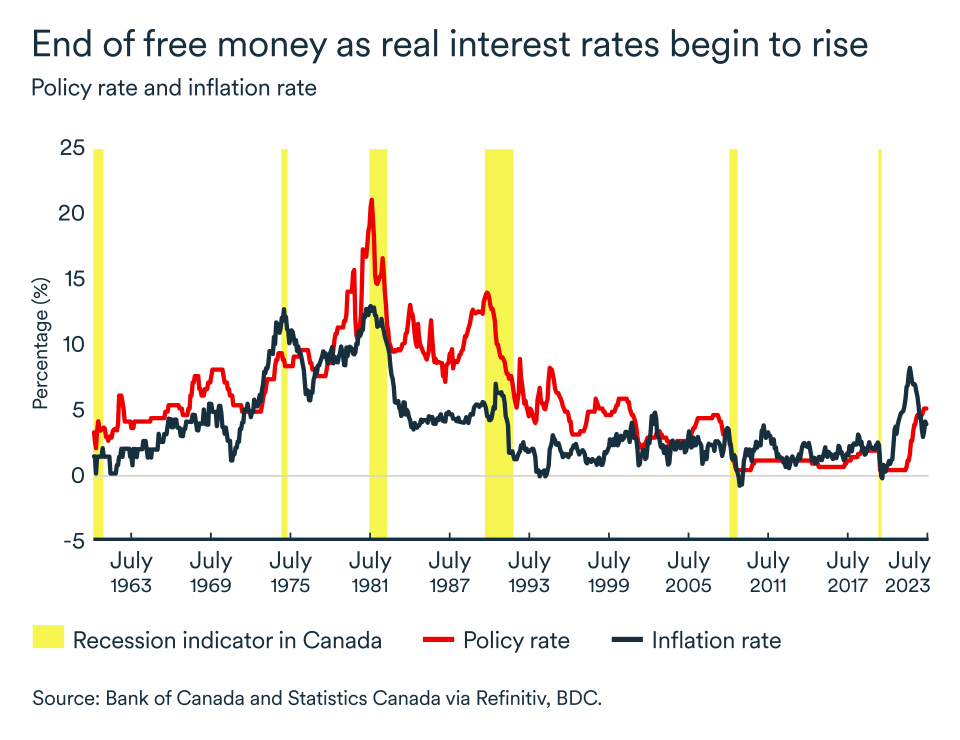

The direction of interest rates depends on the fight against inflation. Even if current high interest rates are a source of frustration and concern for many households and businesses, a policy rate of 5.0% is necessary to restore the balance between supply and demand and achieving long-term price stability.

Tighter credit conditions and the reallocation of household budgets toward debt repayment (mainly mortgage debt) will continue to slow demand in the economy. As a result, inflation should continue to fall over the coming months, but significant gains will be increasingly difficult to achieve.

Enlarge the table

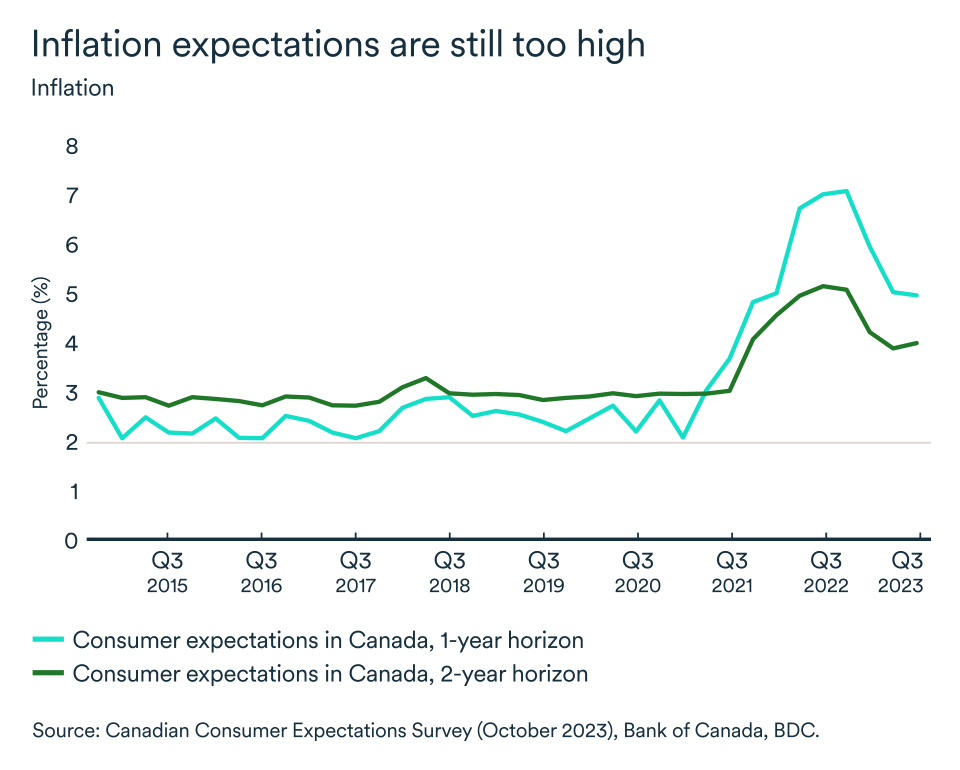

Enlarge the tableConsumer inflation expectations for the coming year are still high at 5.0%. Inflation is a highly self-fulfilling mechanism—the more consumers believe prices will rise, the more they act on that belief by, for example, demanding higher wages.

The Bank of Canada expects inflation to return to 2% by 2025. Does this mean we'll have to wait until then to see our first rate cut? Not necessarily.

Say goodbye to interest rates below 2%

Although the Bank of Canada has given no indication of when or how quickly it will cut rates, at BDC, we believe rates could start to come down as early as the summer of 2024. By then, the economy will have slowed sufficiently for pressure on production capacity to have eased domestically.

However, to reach the inflation target, interest rates will have to remain higher than we had grown accustomed to during the past decade. This is because our economy is subject to multiple constraints that will persist, including an aging population, the reorganization of supply chains following the pandemic, and rising uncertainty and geopolitical risks.

So, we shouldn't expect to see a return to the interest rate that had prevailed since the financial crisis and recession of 2007-2008, when the real rates were negative. (The real interest rate is the nominal rate adjusted to eliminate the effects of inflation, so when the policy rate is lower than the inflation rate, the real interest rate is negative).

Instead, we are likely to see a more gradual reduction in interest rates once inflation has been brought under control. Barring a major, unpredictable shock, the Bank of Canada’s key rate should be on a downward trend by mid-2024, closing the year at around 3.5%.

Ultimately, we expect the bank to bring the policy rate back close to 2.5%—considered the neutral rate—but this is not likely to happen before 2025.

Enlarge the table

Enlarge the tableHere are a few tools to help you navigate high interest rates

- Calculate your company's debt-to-equity ratio, as well as other important ratios that banks take into account when evaluating loan applications.

- The commercial loan calculator is also useful for determining the interest associated with your loan.

The bottom line

- Inflation is on a downward trend, but several factors, including the persistently high expectations of consumers, will make further gains increasingly difficult.

- We expect the Bank of Canada’s key rate to remain at 5.0% for the rest of 2023 and the first half of 2024, with a first downward revision in the summer of next year.

- The bank will not bring its key interest rate close to 2.5%, the neutral rate, until 2025. Therefore, rates will remain higher than those to which Canadians have grown accustomed to over the past 15 years.

- We will have to keep a close eye on wage growth, which could prove to be a major factor in keeping inflation stubbornly high and lead to more rate hikes in Canada.

Post a comment